• 2 min de lectura

• 2 min de lectura

Last updated on 02 Jul, 08:08

Published 02 Jul, 08:08

Contributing author: Yuan Li, Junior Risk & Compliance Analyst at Kpler (yli@kpler.com)

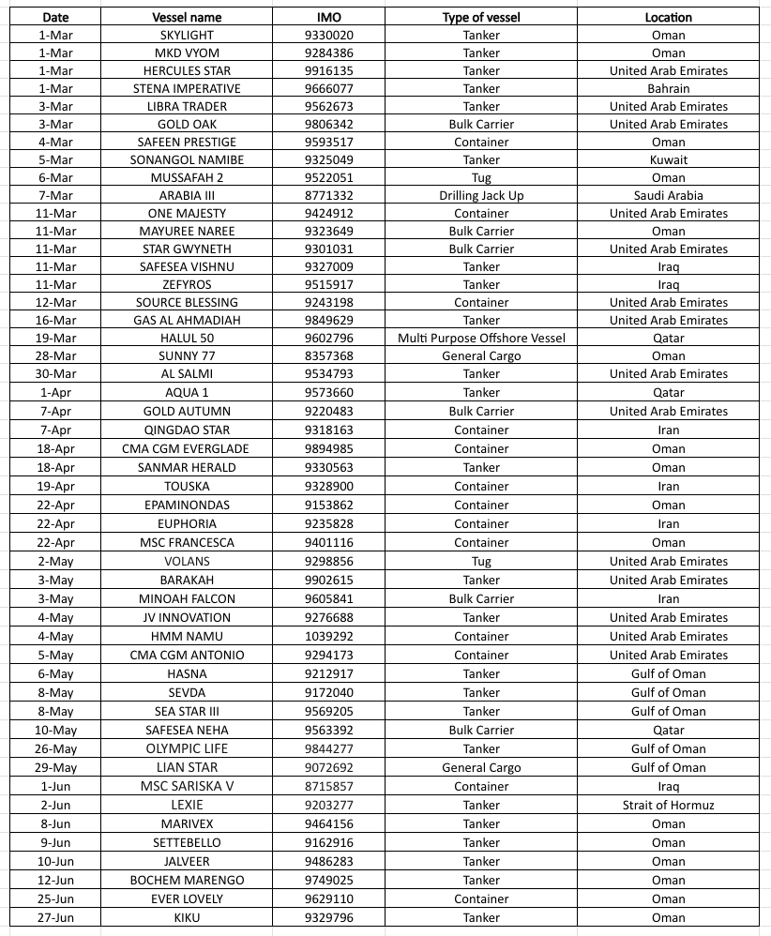

Table of physical attacks on vessels as of July 2 Source: Kpler Risk and Compliance, IMO

Source: Kpler Risk and Compliance, IMO

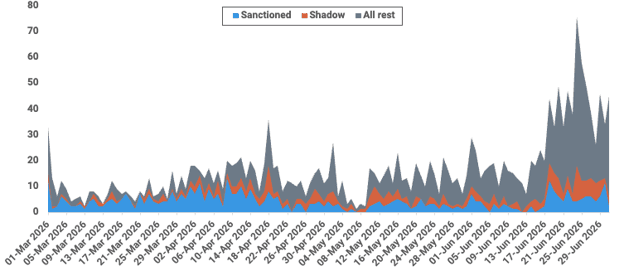

Vessels crossed SOH by risk level as of July 1 Source: Kpler Risk and Compliance

Source: Kpler Risk and Compliance

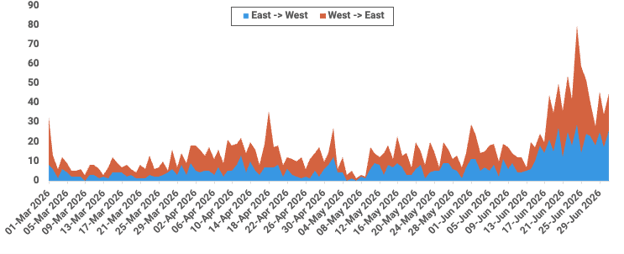

Vessels crossed SOH by direction of crossing as of July 1 Source: Kpler Risk and Compliance

Source: Kpler Risk and Compliance

Confirmed Strait of Hormuz crossings rose d/d to 45 as of 1 July, up from 34 the previous day. Commercial traffic continued to dominate, while low-risk vessels accounted for 39 crossings. Flows were skewed east-west, and only three Iranian-flagged vessels transited. Laden voyages mostly carried CPP, LPG and fertilizer, while non-commercial activity included container ships and general cargo vessels.

Route visibility shifted toward the Omani route, which accounted for 21 crossings, followed by 11 via the Iranian Route and smaller volumes through the Dark/Unknown and IMO routes. The Omani route's stronger representation suggests that operators are gradually testing the alternative corridor after recent demining and coordination efforts, although residual caution remains visible in the continued use of opaque routing. No new physical attacks have been recorded since 27 June, but routing behavior shows that confidence is still conditional rather than fully restored.

Negotiations remain active but unresolved. US and Iranian officials held separate meetings in Qatar and agreed to continue discussions, with Hormuz traffic, route control and Iran's proposed post-interim fees still central to the talks. Iran continues to insist that vessels follow approved routes and has warned of a forceful response against deviations, while the US and Gulf states remain opposed to any tolling or Iranian-controlled passage regime. The read-through for shipping is mixed as the Omani route uptake is a constructive sign (if sustained), but until route governance, fee structures and safe-passage guarantees are resolved, the recovery is likely to remain uneven and vulnerable to renewed disruption.